tinyBuild

Overlooked game pipeline with 300%+ short-term return potential

I like to play the percentages. This mostly means buying predictable businesses with a solid history, trading cheaply, preferably with some economic moat, returning cash to shareholders, with durable cash earnings and significant insider shareholding. If there is an asset-underpin, even better. If you can’t see a way to lose money, that tends to leave just better options. And although I love modelling and forecasting, I try my best to avoid buying things where that is necessary.

Aside from insider ownership and cheapness, this company is almost none of those things. But cheapness is not as obvious here - it needs to be teased out. So why am I wasting my time writing about it? Well, I just think the near-term upside is incredible. And although the company history and industry doesn’t suggest it, the chance of losing money doesn’t seem very big to me. That makes it a highly asymmetric investment opportunity, albeit one with a much wider range of outcomes than I mostly focus on.

The company is tinyBuild and the industry is video game publishing and development. They have built up a large pipeline of high potential indie games over years, many of which are likely to be released in 2026. This pipeline is not currently reflected in the company’s valuation. I’d argue that a company this size (just £30m market cap) should not have such an attractive pipeline. The success of new games is incredibly difficult to predict, but there are metrics we can use to guide us. And since the pipeline is fairly broad (10 announced games), a few failures can be made up for with successes.

By assuming a median outcome for game success, I arrive at a return of almost 300% in just 18 months. That’s my base case. If releases go well, the return could exceed 500% - my upside case. And that’s without a mega-hit on one of their three most promising titles, what I’ve creatively dubbed “The Big Three”. Even in a scenario of unsuccessful game launches across the entire pipeline, one should still make more than 40%.

Sound too good to be true? I must admit that if I had an analyst bring me those projected returns, I’d throw them out. But I’m the analyst, so am unlikely to fire myself. And the combination of a low valuation and no allowance for the earnings boost from the new game pipeline makes these scenarios plausible. There are good reasons for the current lack of investor recognition. Firstly, the company IPO’d at more than 10x its current market cap about 5 years ago, and the share price subsequently collapsed. Secondly, tinyBuild ran out of cash and had to do an emergency equity raise about 2 years ago, diluting existing shareholders and destroying trust. Thirdly, this is a tiny (cough) company with very low liquidity, making it ignored by almost all funds. And finally, it’s the video game industry.

Those are excellent reasons to be skeptical. But given the opportunity for high returns, it may just be worth your while to read on.

Disclaimer: I own shares in tinyBuild, so may be biased. Adjust your views accordingly.

A brief overview of the video game business

Video games come in many shapes and sizes. They are typically categorized as AAA, AA or indie depending on their development budgets. They are released on PC (mostly through Steam) and consoles (Xbox, Playstation and Switch).

A game can retail anywhere from $10 to $80+, with AAA games towards the higher end and indie games towards the lower end of that range. AAA games come with massive development and marketing budgets, but also higher expectations. They can attract millions of players if successful and keep selling for 10 years or more if kept refreshed and updated. And because they cost so much to develop, AAA games take fewer risks with their game concepts and favor what has worked in the past.

Indie games rely more on word-of-mouth and targeted marketing to attract an audience, and are often more innovative in their game concepts. But they can also sell millions of copies if they strike the right chord with players, and even become mainstream. This makes the outcome variance larger for indie games, but they also cost much less to develop ($500k - $5m+) than their AAA counterparts ($50m - $500m+). Players buy indie games because they’re cheap and can be quite unique. The market for AAA games is obviously much larger.

Gamers can be fickle. They can show intense interest in a release and be put off by seemingly small issues. At the same time, perfect games do not exist, and releasing a game that runs smoothly and players want to play is extremely challenging. This all makes the success of a new game unpredictable.

The industry can also be divided into publishers and developers. Publishers will provide funding for game development and marketing in exchange for a revenue share. In a typical agreement, the publisher will fund (some of) the development and share in a third of the proceeds, after they’ve recouped their upfront investment. They will also provide marketing expertise and industry know-how to a game’s release and design. Under these agreements, called 3rd party, the developer will retain the rights to the game’s IP for future use (sequels, media, etc.). Then you get 2nd party agreements which work the same way, except the publisher pays more upfront, retains rights to the IP and shares in about 50% of the proceeds after recouping their upfront investment. Then you get 1st party agreements where the publisher owns the development studio, so owns the game IP and gets the lions share (80%+) of the proceeds.

The industry is fiercely competitive, and global success tends to be concentrated in a few names / titles. But there is still room for indie publishers / developers to make decent returns if run well. And there is always the prospect of a hit game that defies normal expectations.

tinyBuild’s tumultuous history

tinyBuild is a publisher and developer. It was founded by the current CEO, Alex Nichiporchik, off the back of a single game title called No Time To Explain, released in 2011. They are most well-known for their hit franchise Hello Neighbor, first released in 2016, which then evolved into multiple subsequent games and a TV series.

tinyBuild IPO’d in 2021 during the post-COVID tech boom at an eye-popping £340m market cap for £1.69 per share. Alex sold some equity and reduced his stake from 61.1% to 38.2%, pocketing £56m. The IPO also allowed tinyBuild to raise capital of £36m, which they subsequently spent poorly on acquiring new game IP, studios and another 3rd party game publisher company called Versus Evil. As the tech bubble popped and people started to leave their homes after COVID, the demand from the platforms like Xbox and PlayStation dwindled. This reduced tinyBuild’s high margin contracted platform revenue, which placed the company under tremendous financial pressure. They were still funding the development of a large game pipeline, were overstaffed, and their multiple acquisitions were not performing well. This all forced the company to raise $12.3m equity ($11.4m net of fees) at the start of 2024, most of which came from Alex who contributed $10m, increasing his equity stake back up to 57.9%. This equity was raised at just £0.05 per share, 97% below the IPO listing price and diluted existing shareholders by about 50%.

So needless to say, the company has a spotty history and most shareholders have not fared well thusfar. tinyBuild suffered from: a) an incredibly high (unjustified) valuation at IPO during a COVID tech bubble, b) undisciplined corporate spending and terrible acquisitions at high prices, and c) an over-reliance on key platform customers which subsequently disappeared.

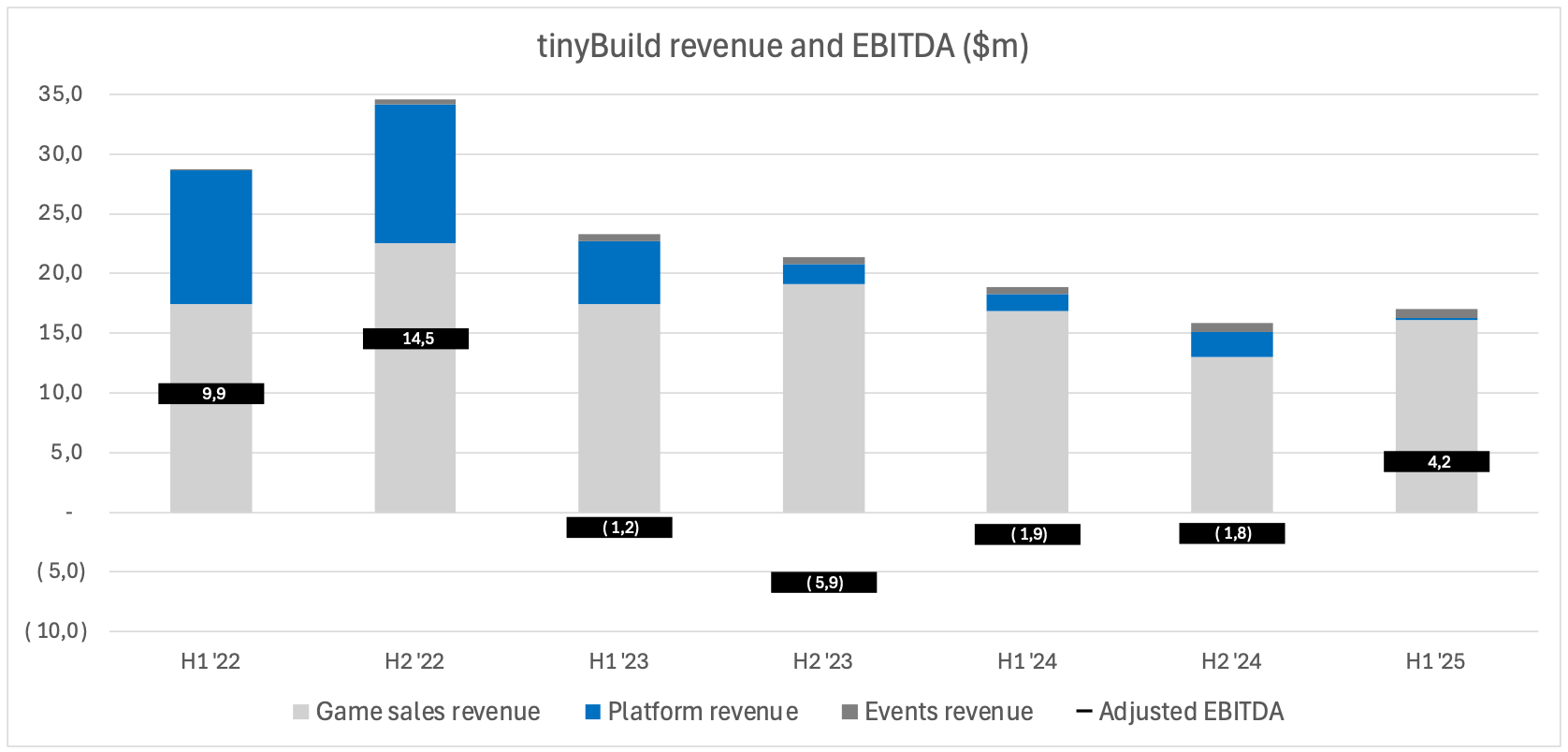

Since the equity raise, tinyBuild have stopped making acquisitions, cut administrative costs, closed Versus Evil, sold some game IP and refocused their pipeline development on the highest potential titles. In the last half-year they’ve become profitable again on an adjusted EBITDA basis, posting $4.2m for H1 of 2025. Their current cash balance sits at $4.6m (no debt), and their software development spend is broadly in line with their cash flow from operations.

*Adjusted EBITDA excludes IPO expenses, one-off legal fees and share-based compensation (which is small), but includes amortization of development costs

The company’s focus is now on 1st party and 2nd party titles. They want to control the IP so that they can leverage successful releases into subsequent games and other media releases (like movies). They spread their development money quite widely, with multiple irons in the fire at any one time. These investments are a mixture of new games and expansions of existing successful games. They’ve had a few recent successful releases as well as a few flops, but the major focus should be on their upcoming game pipeline.

The Big Three

The desirability of upcoming games can be assessed by their wishlist rankings. Players add games to their wishlists on Steam based on trailers, reviews, demos, playtests or word-of-mouth recommendations. Think of a wishlist as a shopping cart, and when items in the cart become available or go on sale, the player is notified via email. Steam then ranks all of the upcoming games according to the number of players that have added them to their wishlists. The more desire the gaming community has to play an upcoming game, the higher it is in the wishlist rankings.

AAA games with bigger budgets tend to be higher in the wishlist rankings. This is because their publishers can spend more money on marketing, they are visually more appealing given the money spent to develop them, and they are often sequels to existing games with loyal fan bases of players. But from time to time, indie games strike a chord with players and also make it high up in the rankings. tinyBuild currently has three such games.

Kingmakers is currently ranked #5 (of all upcoming games globally), with an estimated 1.4m people having added the game to their wishlists. The game exploded in popularity when its release trailer went viral at the start of 2024. The concept is unique: a modern soldier takes modern weapons back in time to turn the tide of medieval conflicts and change history. Think Back To The Future meets Rambo. The engineering / development behind the game also appears novel, allowing hundreds of characters on the screen without placing too much strain on computing systems. The virality of the game trailer has resulted in Netflix teaming up with Story Kitchen (a production company specializing in adapting video games into film, with titles like Tomb Raider) to make a Kingmakers movie. This is being done before the game has even been released. Since tinyBuild are engaging with Netflix and Alex is the executive producer on the movie, it suggests that they own the IP, likely making this a 2nd party title. It’s not clear at this stage whether the movie will make money for tinyBuild or just act as fantastic marketing for the game. But as a game, Kingmakers has incredible potential and could easily justify tinyBuild’s current market cap on its own.

Sand: Raiders of Sophie is currently ranked #38 on Steam’s rankings with an estimated 750,000 people having added the game to their wishlists. The game is a multiplayer extraction shooter set in a desert world where players build tramplers (giant walking desert “ships”) to fight against each other. The game has gone through multiple playtests and has clearly resonated with audiences. tinyBuild are planning to release the game on consoles at the same time as its Steam release, which increases its initial sales potential (although costs more money to develop). The game is being developed by an internal team at tinyBuild, making it a 1st party title.

Streets of Rogue 2 is a sequel to Streets of Rogue, which has sold more than 1m copies since 2019 with 96% positive ratings. Sequels have dedicated fan bases, increasing their likelihood of success. With over 600,000 wishlists, the game currently ranks #76 on Steam. The game is described as an RPG Sandbox set in a vast randomly generated open world, and appears to be an ambitious expansion of the original title. The game was originally set to be released in 2024, but has seen long delays. It is being developed by a single developer, which reduces the cost to produce the game but also lengthens the development timeline. Given the lengthy delays and lack of clear guidance, this game has the least clear release timeline of The Big Three. tinyBuild acqui-hired the maker of Streets of Rogue, so it owns the game IP and the developer works for them. This increases the game’s revenue share as a 1st party title.

Pipeline forecasts and potential investment returns

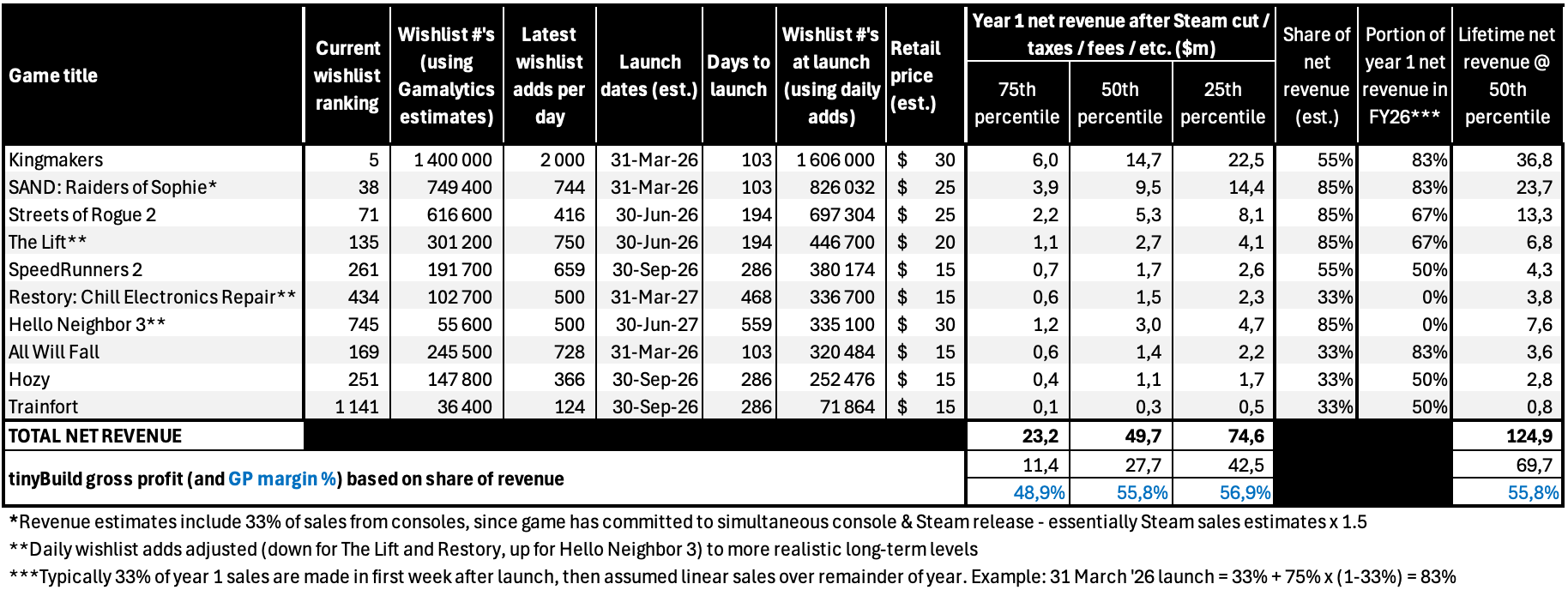

In order to quantify the value of tinyBuild’s pipeline, one needs to estimate how much each game could make for tinyBuild. The following table shows my estimates of the pipeline game revenue and gross profit in the first year after release, based on the current wishlist numbers and trajectory to launch.

There is a lot of detail in this table, and since it forms the crux of my estimates for FY26 earnings, I will discuss the components one by one. Although the detail may give the impression of precision, this should not be your take-out from this table. It is meant to give an indication of the range of potential outcomes. So working from left to right in the table:

Since we only have today’s wishlists, I’ve used the current daily wishlist additions to estimate the wishlists at launch, based on when I expect each game to be released.

Release dates are uncertain. Even when a game announces an actual date, that date can change. Game development timelines are inherently difficult to estimate, even for the actual developers. Besides development, there are other factors that play a role in release dates moving, notably the release dates of other major (or just similar) games. The concern is that another extremely popular game can suck the attention away from your game if released at the same time. And the initial sales of a game are crucial to its long-term success. So sometimes developers purposely delay their releases so as not to clash with another highly anticipated bigger budget title that has more marketing dollars behind it. This may have been part of the reason for delaying Kingmakers, which was originally scheduled for 8 October 2025, with AAA game Battlefield 6 coming out on 10 October.

My estimates for release dates are based on following each game. The most important ones are The Big Three, so I’ll discuss each in turn below. But for overall context its important to note that the release date for GTA 6 is 19 November 2026. This is one of the most highly anticipated games to be released this decade. It will sell millions of copies. TinyBuild is acutely aware of this. Alex has already joked about it on Twitter saying everyone will now announce May 2026 release dates. I don’t think tinyBuild will release any major title in the second half of 2026. They’d want to give any new game several months of runway to build a following before being drained of attention by GTA 6. That may not apply to smaller titles towards the bottom half of the table, but I think it does apply to The Big Three. So given how far the development is for The Big Three, and that they’ve all had previous release dates which were then moved, I think its likely we see them released in H1 2026.

Kingmakers was scheduled for 8 October 2025. When it was delayed, one of the developers on Discord said he favored a Q1 2026 release. They also said the game was 85% - 90% complete at the time. This is the game with the most potential in tinyBuild’s pipeline, so tinyBuild do not want it to come close to the GTA 6 release. Additionally, its probably the most expensive title in the pipeline from a development cost perspective, so I don’t think tinyBuild want to spend another year on the game and release it in 2027. End of Q1 2026 seems like a good estimate given the above.

Sand: Raiders of Sophie was previously announced for 3 April 2025. The game has since done two open playtests in August and October, giving the developers the opportunity to test and tweak the game. Then two weeks ago they announced the release for Q1 2026. Note that the Sand release will be a simultaneous PC and console release. This is unusual as console ports are costly and tinyBuild usually want to test how well a game is received before porting it to consoles. But for Sand they decided to do both at once. This probably doubles its revenue potential since consoles sales are normally similar to PC sales, although I’ve assumed just 33% of sales come from console for conservatism. (Note the wishlist numbers shown are only for Steam)

Streets of Rogue 2 was originally planned for release in October 2024. But bugs combined with a lack of content has resulted in solo-developer Matt Dabrowski pushing the release out to 2026. I think mid 2026 is probably reasonable. Again, I think GTA 6 will make H1 2026 the most likely time period for release. Matt has even publicly joked about releasing the game before GTA 6 a few times.

The retail price for games depends on what other similar games are priced at and the amount of money spent on development. To entice players to buy them, indie games will always be priced well below AA and AAA titles that come out at $50 - $80. TinyBuild’s games typically have a floor of $15, and a ceiling of $35. Kingmakers was rumored to be priced at $27 - $35 at release (before it was delayed) with a cap of $40. Sand and Streets of Rogue 2 are both slightly more premium titles than average, and given Streets of Rogue (the original) is $20 I think those two games come in at $25. These price estimates may be off, but its unlikely they’re wrong by more than $5. I’ve tried to be conservative in my estimates.

The year 1 net revenue estimates are based on each game’s wishlist numbers at launch and the game’s retail price. There is a strong correlation between a game’s wishlist numbers and the number of copies it will eventually sell, with a swing factor being the game’s quality. The correlation between wishlist numbers and copies sold have been studied by sites like impress.games based on thousands of games released, and then used to produce calculators for developers to use to estimate game sales. That tool is freely accessible. Since we don’t know whether a game will deliver on its pre-launch promise, I’ve used three outcomes: a 75th percentile - where 75% of games perform better at converting wishlists to sales, a 50th percentile (the median), and a 25th percentile. See this as a bad outcome, an average outcome and a good outcome respectively, given each game’s wishlists at launch. Wishlist figures can be accurately estimated from Steam’s wishlist ranking and be found for each game on sites like gamalytic.com.

I apply a share of net revenue (with the developer) to the net sales to get the gross profit contribution. For the top four games, tinyBuild owns the game IP. They also own the studios behind Sand and The Lift, and “acqui-hired” Streets of Rogue 2 in 2022 implying they employ Matt Dabrowski. This probably puts their revenue share at 80%+ for those titles. The movie for Kingmakers suggests tinyBuild owns the IP, making it a 2nd party title. For Hello Neighbor 3 they own the IP and studio, and they own the IP on SpeedRunners 2. I’ve assumed the rest are 3rd party titles where tinyBuild gets 33% of profits after recouping their upfront investment.

The gross profit from new games drops to the EBITDA line for tinyBuild, since the admin expenses are more-than covered by the existing (back catalogue) game sales. These total gross profit figures can then be used to estimate earnings for FY26 shown below.

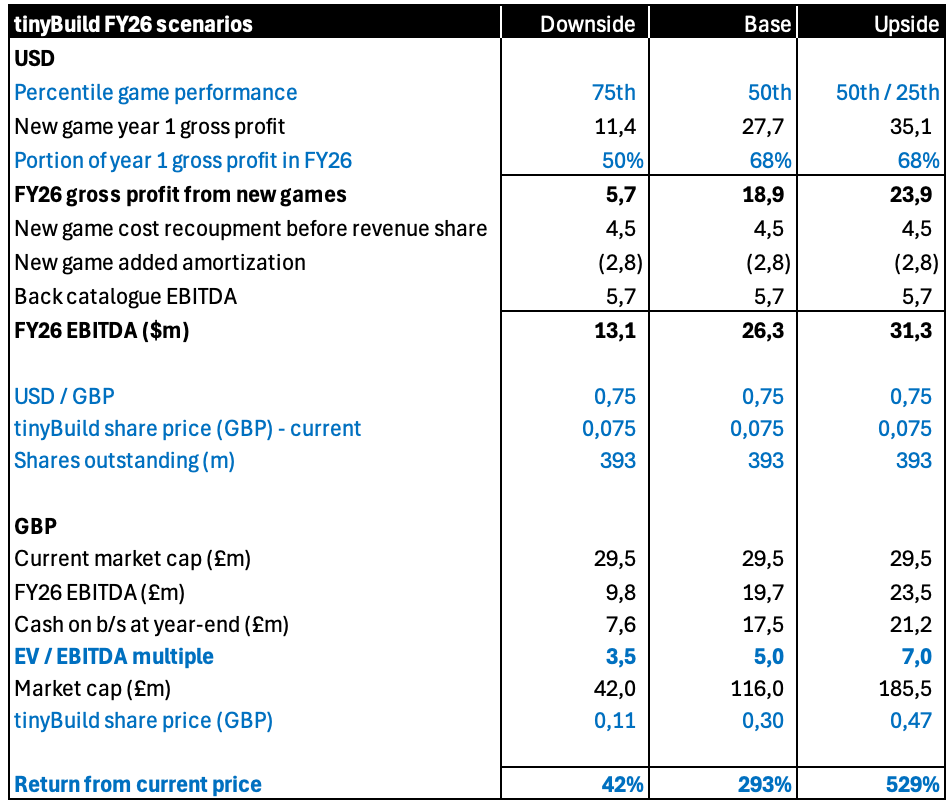

The three scenarios assume different percentiles of outcomes for the games pipeline from the previous table. The upside case uses a 50/50 split between the median and the 25th percentile columns.

You may have noticed that most games only get released part-way through the year, so counting their full 1-year gross profit contribution would overstate earnings. I’ve applied a proportion of the year 1 pipeline gross profit to arrive at FY26 estimates. If all goes according to the assumptions then we should get 68% of year 1 revenue landing in FY26. (Note that a game typically earns 1/3rd of its year 1 sales in the first week after release, so release timing only really affects the timing of 2/3rds of the year 1 gross profit.)

I’ve estimated tinyBuild’s upfront cost recoupment from each game as well as the increased game amortization (which is included in their EBITDA, despite being amortization). Both depend on the individual game development budgets which we don’t know for sure, but it’s not a major swing factor and they partly cancel each other out. This is then added to my estimate of their back catalogue EBITDA (from current games) which I’ve assumed comes down from $8m - $10m in FY25, to just under $6m in FY26 as those games age.

The EBITDA is then converted into pounds, to which the balance sheet cash is added. I’ve assumed the cash is equivalent to the new game gross profit plus upfront cash recoupment of development costs from those games, with current cash plus back catalogue EBITDA used to fund ongoing capex (as it currently does).

The EBITDA multiple I’ve used depends on the scenario. Currently I estimate the multiple to be between 4x and 5x FY25 EBITDA. I’ve used 5x in the base case, despite competitors currently trading at 10x EBITDA or higher. Competitors are larger companies and tinyBuild does have a spotty track record so I think conservatism is warranted. I prefer not relying too much on high exit multiples for my investment theses. Even the 7x multiple on the upside case is arguably on the low side.

As you can see, the returns are exceptional over a short time-frame. This is driven by a long-awaited games pipeline finally coming to fruition. To fully realise these returns, one would likely need to wait until the FY26 financial results are announced in April 2027. But the actual game sales can be monitored as soon as each game is released. This allows one to track the thesis closely.

What could go wrong?

The company could run out of cash before the games come out.

This was a greater concern 6 and 12 months ago. They seem to have got their spending under control and more aligned with their game revenue. They’re more cautious with their capex spending on new games. But having said all this, they ran out of cash before. No institution is going to lend them money if they run short. I don’t think they will run out of cash, otherwise I wouldn’t be invested. I am relying on the CEO’s significant equity stake and a newfound conservatism born from their brush with bankruptcy, and a recent track-record of generating positive cash flow. They now have $4.5m on the balance sheet. Also in their favour are the recent releases of The King is Watching and Of Ash and Steel, both of which are selling well and will add to tinyBuild’s cash pile.

Their new games could flop.

This would really hurt prospective earnings if the flops were for one of The Big Three. Games have flopped before. Recent examples of large flops are:

Broken Roads was a highly anticipated game with large wishlist following, but released in April 2024 with too many bugs, boring gameplay and not enough content. The game reviews were extremely poor and sales quickly dried up after launch. Admittedly this was a game that tinyBuild took over as the publisher from Versus Evil quite late on leaving little time for adjustments. Little else at Versus Evil seemed to be managed very well from when tinyBuild acquired them, and this game was no exception.

Level Zero: Extraction was keenly anticipated and showed great promise during its playtests. The game released in August 2024 to an eager audience. But the asymmetric game design just put too many people off, which drove down the review scores and killed new sales. Since the game was a multiplayer title and needed many players to keep filling up new games, the game lobby dried up. This same thing could happen to Sand since it is a multiplayer extraction shooter.

FEROCIOUS is a first-person shooter exploration game involving dinosaurs that launched just a few weeks ago. The game was release with more than 400,000 wishlists, but sales have been extremely disappointing. Some of this can be attributed to plenty of bugs in a game that was claiming to be fully developed (not early access), which led to very negative early reviews. The impact from negative early reviews was likely compounded by a late release time – possibly a communication mistake with Steam which had an earlier time on their site. This may have delayed some early adopter sales. But overall the extremely poor sales are difficult to explain given the number of wishlists, putting the outcome near the 90th percentile. I doubt this game covers its development costs.

These flops should be viewed wholistically. Consider the recent successes:

The King Is Watching released in July 2025 and has already sold more than 400,000 copies as per a Twitter post a few weeks ago. Given that it had less than 250,000 wishlists at launch, that puts it above the 10th percentile in terms of outcomes from its wishlists at launch. Critically this is a 1st party title developed internally at tinyBuild, which means that the revenue share for the company will likely be 80%+.

Of Ash and Steel released in November 2025. The game had about 300,000 wishlists at launch. The game released with plenty of bugs, but there was clearly a yearning for this type of old-school role-playing game. So despite a low review score in the 60s, the game seems to be selling quite well. We don’t have an official sales figure yet, but I estimate an outcome above the 25th percentile given its review count and wishlists at launch. They just released a patch to fix many of the bugs, and so far the subsequent review scores have been excellent at 90%+ positive.

VOIN is a hack-and-slash game developed by a solo-developer which was released in December 2024. The game has 94% positive reviews and has estimated sales of more than 100,000. Given it had just 130,000 wishlists at launch, that’s an outcome in line with the 25th percentile.

So predicting the outcome of any one game is very difficult. Wishlists give us a guide, but buggy games, negative early reviews or poor game design can quickly result in a game disappearing into the black hole of failed titles. These bad outcomes can be balanced out by very good outcomes which can be equally unexpected. This lack of predictability for a new games is precisely what makes game developers / publishers lower quality from an investment perspective. tinyBuild’s game pipeline does contain 10 titles, 3 of which have great potential. This helps to diversify the risk of flops. One should therefore consider the pipeline as a whole. And of course, there is always the possibility of a mega-hit which would make smaller flops largely irrelevant.

The games could do well, but management then does bad (value-destructive) things with all the excess cash. I think this is quite possible. They’ve done this before, when they raised a lot of cash during the IPO and then blew much of it with little to show for the spend. I’ve never been enamored with management’s capital allocation skills. They ran out of cash after having raised a lot of it not long before, which shows a degree of recklessness. Alex is a game developer at heart, and good capital allocation is a skill lacking in some of the largest businesses filled with finance professionals. So this is a risk I’m quite concerned about.

Don’t get me wrong, the pipeline of games they’re currently invested in looks very good. But the chance they replicate that once they have more cash to play with seems too small for my liking. The temptation to spend lots of cash on “expensive shiny new toys” doesn’t inspire the discipline I’d want to see. However, this is a risk I think I can manage. If the games come out I will look at how they’re selling. I will then compare that to how the share price performs. If I think that the share price reflects much (or even just some) of the prospective earnings, then I’ll look to sell down my stake significantly. In a way, many of the games being delayed to 2026 is a good thing. Since most are likely to release in FY26, I’ll have a clearer idea of where things stand by year-end, especially once FY26 earnings are out in early 2027. This should not give management much time to commit to new titles (ie. spend the cash). I can then take some money off the table and derisk the position.

Game releases could be delayed.

Thus far this has happened to The Big Three, so could certainly happen again. A delay of one of the big games would delay, rather than kill, the thesis. So although I think this is quite possible, it merely lengthens the investment timeline rather than resulting in an investment loss. I do think that GTA 6 coming in late 2026 compresses the release window for many of the titles in H1 2026. But some of the games could always be pushed into 2027.

A wide range of great outcomes from an unpredictable business

tinyBuild looks to have turned a corner with its latest earnings. There is still a shadow of the past hanging over the share, which makes it trade below 5x my estimate of FY25 EBITDA. But I think this shadow can be dispelled with strong releases in 2026. The game pipeline appears extremely valuable, so not only does an investor today get tinyBuild at a low price, this price hardly seems to place any value on the pipeline. Kingmakers in particular has amazing potential, highlighted not only by a top 5 ranking in the wishlists, but by Netflix picking up the title despite the game not even having been released yet.

But buyer beware. Games flop. Success is unpredictable. tinyBuild has run out of money before. There are no guarantees of success. But I think the odds are very much in one’s favour here, and the payoff for success is exceptional. And as shown, even in a bad outcome across the pipeline with a low multiple, the returns are pretty good.